Classification of Banking Industry.

Indian banking industry has been divided into two parts, organized and unorganized sectors. The organized sector consists of Reserve Bank of India, Commercial Banks and Co-operative Banks, and Specialized Financial Institutions (IDBI, ICICI, IFC etc.). The unorganized sector, which is not Indian Banking System homogeneous, is largely made up of money lenders and indigenous bankers.

An outline of the Indian Banking structure may be presented as follows:-

1. Reserve banks of India.

2. Indian Scheduled Commercial Banks.

a) State Bank of India and its associate banks.

b) Twenty nationalized banks.

c) Regional rural banks.

d) Other scheduled commercial banks.

3. Foreign Banks

4. Non-scheduled banks

5. Co-operative banks.

Reserve Bank of India:

- The reserve bank of India is a central bank and was established in April 1, 1935 in accordance with the provisions of reserve bank of India act 1934.

- The central office of RBI is located at Mumbai. since nationalization in 1949, RBI is fully owned by the Government of India. It was inaugurated with share capital of Rs. 5 Crores divided into 11 shares of Rs. 100 each fully paid up.

- The RBI Act 1934 was commenced on April 1, 1935. The Act, 1934 provides the statutory basis of the functioning of the bank. The bank was constituted for the need of following:-

- To regulate the issues of banknotes.

- To maintain reserves with a view to securing monetary stability-

- To operate the credit and currency system of the country to its advantage.

Functions of RBI:

Bank of Issue: The RBI formulates, implements, and monitors the monetary policy. Its main objective is maintaining price stability and ensuring adequate flow of credit to productive sector.

Regulator-Supervisor of the financial system: RBI prescribes Indian Banking System parameters of banking operations within which the banking and financial system functions. Their main objective is to maintain public confidence in the system, protect depositor’s interest and provide cost effective banking services to the public.•

Issuer of currency: RBI issues and exchanges or destroys the currency and coins that are not fit for circulation. His main objective is to give the public adequate quantity of supplies of currency notes and coins and in good quality.

Developmental role: The RBI performs the wide range of promotional functions to support national objectives such as contests, coupons maintaining good public relations and many more.

Controller of Credit: RBI performs the following tasks:

- It holds the cash reserves of all the scheduled banks.

- It controls the credit operations of banks through quantitative and qualitative controls.

- It controls the banking system through the system of licensing, inspection and calling for information.

- It acts as the lender of the last resort by providing rediscount facilities to scheduled banks.

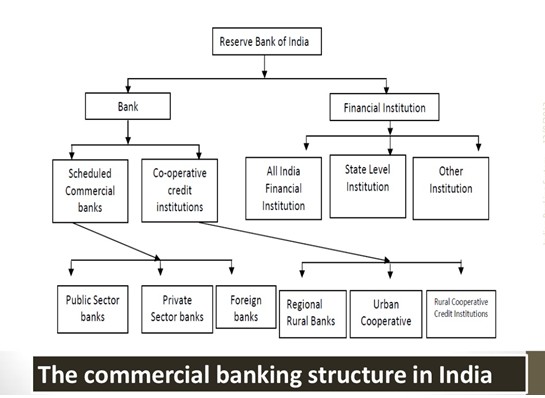

The commercial banking structure in India

Indian Scheduled Commercial Banks.•

COMMERCIAL BANK– An institution which accepts deposits, makes business loans, and offers related services. Commercial banks also allow for a variety of deposit accounts, such as checking, savings, and time deposit. These institutions are run to make a profit and owned by a group of Indian Banking System individuals, yet some may be members of the Federal Reserve System. While commercial banks offer services to individuals, they are primarily concerned with receiving deposits and lending to businesses.

The commercial banking structure in India consists of scheduled commercial banks, and unscheduled banks.

Scheduled Banks: Scheduled Banks in India constitute those banks which have been included in the second schedule of RBI act 1934.

- Scheduled bank are those banks whose minimum paid up capital and reserves are not less than 25 lakhs.

- Scheduled banks in India means the State Bank of India constituted under the State Bank of India Act, 1955 a subsidiary bank as defined in the State Bank of India Act, 1959 (38 of 1959), a corresponding new bank constituted under section 3 of the Banking companies Act, 1980.

- Private sector, Public sector, and Foreign banks come under the umbrella of scheduled commercial banks.

Unscheduled Banks: “Unscheduled Bank in India” means a banking company as defined in clause (c) of section 5 of the Banking Regulation Act, 1949, which is not a scheduled bank”.

Commercial banks, which dominate this industry, offer a full range of services for individuals, businesses, and Indian Banking System governments. These banks come in a wide range of sizes, from large global banks to regional and community banks.

Regional Rural Banks were set up on October 2, 1975. The banks provide credit to the weaker sections of the rural areas, particularly the small and marginal farmers, agricultural labourers and small entrepreneurs.

Co-operative Banks.

Co-operative Banks Role in rural financing continues to be important even today, and their business in the urban areas also has increased phenomenally in recent years mainly due to the sharp increase in the number of primary co-operative banks. While the co-operative banks in rural areas mainly Indian Banking System finance agricultural based activities including farming, cattle, milk, hatchery, personal finance etc, along with some small scale industries and self-employment driven activities, the co-operative banks in urban areas mainly finance various categories of people for self- employment, industries, small scale units, home finance, consumer finance, personal finance, etc. Example of co-operative banks – Saraswat Co-operative Bank , Jankalyan Sahakari Bank etc.

Tools to Credit Control by RBI.•

Cash Reserve Ratio– Cash reserve Ratio (CRR) is the amount of funds that the banks have to keep with RBI. If RBI decides to increase the percent of this, the available amount with the banks comes down. RBI is using this method (increase of CRR rate), to drain out the excessive money from the banks

Repo Rate- Whenever the banks have any shortage of funds they can borrow it from RBI. Repo rate is the rate at which our banks borrow money from RBI. A reduction in the repo rate will help banks to get money at a cheaper rate. When the repo rate increases borrowing from RBI becomes more expensive.

Reverse Repo Rate– Reverse Repo rate is the rate at which Reserve Bank of India (RBI) borrows money from banks. Banks are always happy to lend money to RBI since their money are in safe hands with a good interest. An increase in Reverse repo rate can cause the banks to transfer more funds to RBI due to Indian Banking System this attractive interest rates. It can cause the money to be drawn out of the banking system. Due to this fine tuning of RBI using its tools of CRR, Bank Rate, Repo Rate and Reverse Repo rate our banks adjust their lending or investment rates for common man.

SLR Rate– SLR (Statutory Liquidity Ratio) is the amount a commercial bank needs to maintain in the form of cash, or gold or govt. approved securities (Bonds) before providing credit to its customers. SLR rate is determined and maintained by the RBI (Reserve Bank of India) in order to control the Indian Banking System expansion of bank credit .

Bank rate-Bank rate is also called as the discount rate. It is the rate of interest which a central bank charges on the loans and advances provided to commercial banks.

Classification of Banking Industry in India